First Majestic Announces Financial Results for Q4 and Year End 2013

February 26, 2014

FIRST MAJESTIC SILVER CORP. (AG: NYSE; FR: TSX) (the “Company” or “First Majestic”) is pleased to announce the consolidated financial results for the Company’s fourth quarter and year ended December 31, 2013. The full version of the financial statements and the management discussion and analysis can be viewed on the Company’s web site at www.firstmajestic.com, on SEDAR at www.sedar.com and EDGAR at www.sec.gov.HIGHLIGHTS

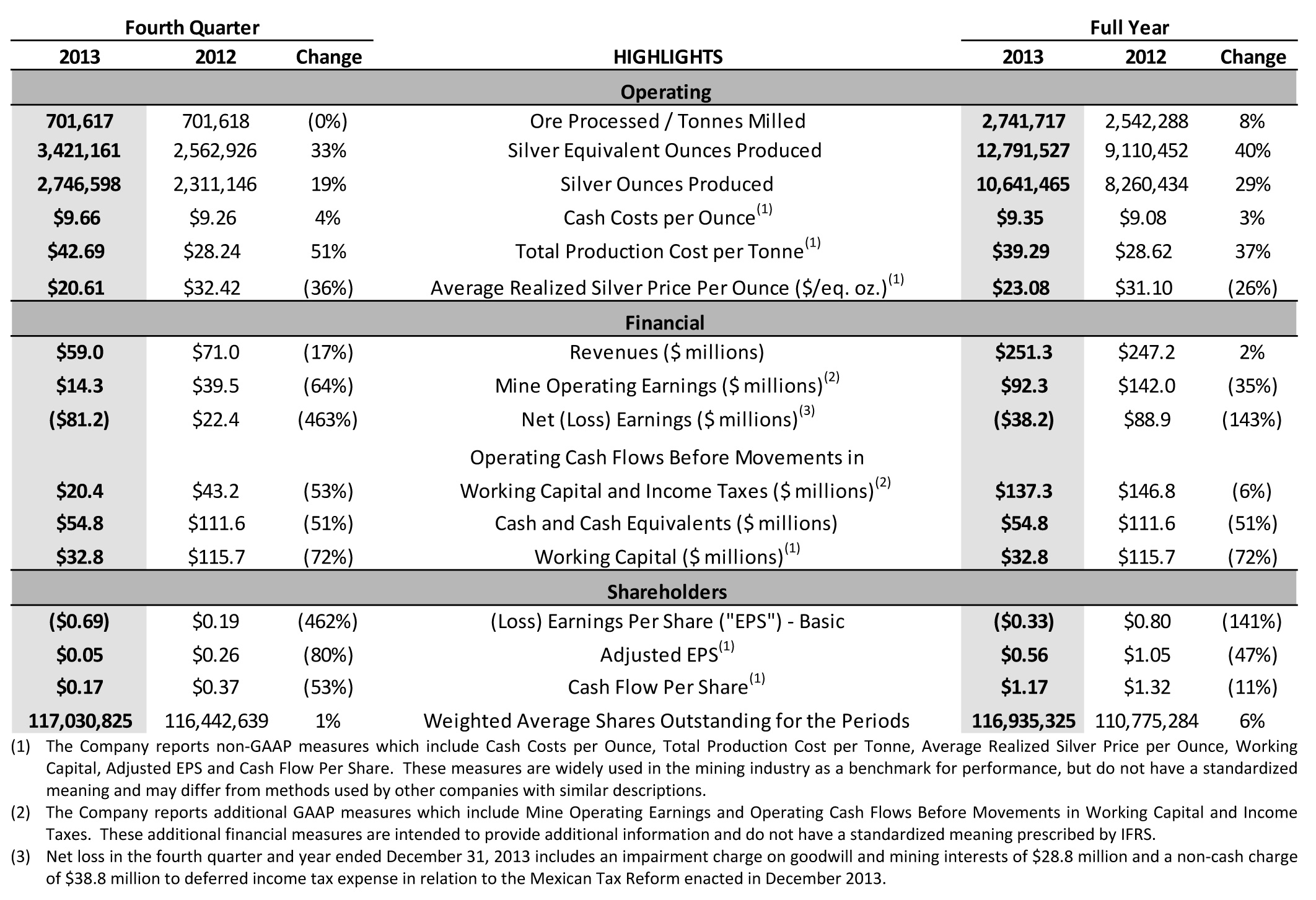

- Silver equivalent production of 3.4 million ounces in Q4 2013, representing a 33% increase from Q4 2012; Full-year silver equivalent production of 12.8 million ounces, representing a 40% increase compared to 2012.

- Silver production of 2.7 million ounces in Q4 2013, representing a 19% increase from Q4 2012; Full-year silver production of 10.6 million ounces, representing a 29% increase compared to 2012.

- Achieved “Senior Silver Producer” status by exceeding the production threshold of 10 million ounces of pure silver.

- Revenues after smelting and refining costs amounted to $59.0 million in Q4 2013; Full-year revenues were $251.3 million representing a 2% increase compared to 2012 despite a 26% decline in average realized silver price.

- Adjusted net earnings (non-GAAP) normalized for non-cash or unusual items was $6.3 million or $0.05 per share in Q4 2013; Full-year adjusted net earnings was $65.1 million or $0.56 per share in 2013.

- Reported net loss of $81.2 million in Q4 2013 after a non-cash impairment charge of $28.8 million and a deferred tax accounting adjustment of $38.8 million as a result of the recently enacted Mexican Tax Reforms.

- Cash flow of $0.17 per share (non-GAAP) in Q4 2013; Full-year cash flow per share of $1.17 in 2013.

- Total cash cost of $9.66 per payable silver ounce in Q4 2013; Full-year cash cost of $9.35 per payable silver ounce.

- Successfully completed three separate expansion projects in 2013 ensuring future production growth plans remain intact.

“The Company continues to focus on operational efficiency, to optimize the mines to ensure profitability in a low price environment. These modifications are aimed to maintain First Majestic as one of the silver industry’s purest and highest margin producers.”

2013 ANNUAL AND FOURTH QUARTER HIGHLIGHTS

FINANCIAL RESULTS

The Company generated revenues of $59.0 million in the fourth quarter of 2013, a decrease of $12.0 million or 17% compared to $71.0 million in the fourth quarter of 2012. Revenues during the full-year 2013 were $251.3 million, an increase of $4.1 million compared to $247.2 million in 2012, as record production in 2013 resulted in 41% increase in payable equivalent silver ounces sold. However, the increase in ounces sold was offset by a 26% decrease in average realized silver price per ounce compared to 2012.

Due to the current metal price environment, the Company decided to take non-cash impairment charges totalling $28.8 million consisting of $24.6 million impairment of goodwill and $4.2 million of impairment charges on the exploration properties acquired from Silvermex Resources Inc.

Net loss after taxes for the fourth quarter and year ended December 31, 2013 were $81.2 million and $38.2 million respectively, compared to net earnings after taxes of $22.4 million and $88.9 million in the comparative periods of 2012. Net loss in the current period was attributed to the non-cash impairment charges and a non-cash accounting adjustment of $38.8 million to deferred income tax liabilities as a result of the recently enacted Mexican Tax Reforms. For the purpose of the impairment charge, the Company used a long-term silver price of $22.30 per ounce and discount rates ranging from 9% to 11%, equivalent to the Company’s weighted average cost of capital, adjusted for specific project risks.

Mine operating earnings were $14.3 million in the fourth quarter of 2013 compared to $39.5 million in the fourth quarter of 2012. The Company recognized mine operating earnings of $92.3 million in 2013, a decrease of 35% compared to $142.0 million in 2012. The decrease in mine operating earnings was primarily attributed to the decline in average realized silver price per ounce during the year. Depletion, depreciation and amortization expense increased by $17.9 million due to an 8% increase in tonnage milled and additional depreciation and amortization from the new Del Toro mine and full year of La Guitarra operations.

During 2013, the Company invested $178.7 million in the development and exploration of its mineral properties, construction of new processing plants and acquisitions of new mining equipment. As previously announced, the Company plans to invest a total of $106.0 million in 2014 on sustaining capital for current operations and expansionary capital for numerous growth projects. The 2014 annual budget implies an estimated 41% reduction in total capital expenditures following the completion of numerous capital intensive growth projects in 2013 including the investment of $122.5 million at Del Toro on the construction of the dual-circuit mill, acquisition of mining equipment and underground mine development, $8.1 million invested at San Martin to increase the plant’s capacity to 1,300 tonnes per day (” tpd”) and $4.3 million invested at La Guitarra to increase the plant’s capacity to 500 tpd.

OPERATIONAL RESULTS

On January 14, 2014, the Company announced its fourth quarter silver equivalent production increased to a record 3,421,161 ounces, an increase of 2% compared to 3,370,457 ounces in the previous quarter. Compared to the same quarter of the prior year, silver equivalent production increased by 33% primarily attributed to additional production from Del Toro, the successful plant expansion at La Guitarra and the improved head grades and tonnage milled at La Parrilla and San Martin.

The overall average head grade for the fourth quarter of 2013 was 191 grams per tonne (“g/t”), a 9% increase compared to 176 g/t in the fourth quarter of 2012 and a 5% decrease compared to 202 g/t in the third quarter of 2013. The increase from the same quarter of the prior year was primarily attributed to 24% increase in head grades from La Encantada due to a higher proportion of fresh ore being processed, 15% higher grades from San Martin, offset by 50% lower head grade from the La Guitarra mine as production ore came from areas within the La Guitarra vein which contained higher gold grades in conjunction with lower silver grades.

Consolidated cash costs per ounce in the fourth quarter were $9.66 compared to $8.84 in the third quarter of 2013 and $9.26 in the fourth quarter of 2012. The increase in cash cost per ounce compared to the prior quarter was primarily attributed to additional diesel and generator rental costs incurred at Del Toro due to delays in the construction of the new 115kV power line and higher than expected smelting and refining costs due to penalties for impurities as the mill was refining its metallurgical processes during the ramp up of this new mine. Additionally, lower recoveries and grades at San Martin resulted in higher cash costs during the fourth quarter. However, with steady production growth anticipated over the next few quarters coming from Del Toro’s cyanidation circuit ramp-up to 2,000 tpd and along with San Martin’s ramp- up to 1,300 tpd, cash costs per ounce are projected to decrease as additional ounces are produced.

Combined recoveries of silver for all mines in the fourth quarter were 64%, an increase of 9% compared to 58% in the fourth quarter of 2012, and remained relatively unchanged compared to 65% in the third quarter of 2013.

In the fourth quarter of 2013, a total of 8,324 metres were drilled over 89 holes consisting primarily of definition drilling and surface exploration drilling, representing a 6% increase from the 7,823 metres drilled in the third quarter of 2013 and 68% decrease from the 25,940 metres drilled in the fourth quarter of 2012. For the year ended 2013, a total of 58,578 metres were drilled compared to 135,769 metres drilled in 2012. As previously indicated, since the second quarter, the Company has been reducing its drilling program, with the majority of metres planned to be drilled by the Company’s own personnel and equipment for the support of mining production, as well as on preparing resource estimations for the future NI 43-101 Technical Reports. There are currently nine active drill rigs at the Company’s five operating mines, four of which are located at the La Encantada mine. The reduced drilling program is expected to delay the release of the planned NI 43-101 Technical Report updates to late 2014.

MINE OPERATIONS

Del Toro Silver Mine

Total production at Del Toro was 693,561 equivalent ounces of silver in the fourth quarter, which was an increase of 22% compared to 567,723 equivalent ounces in the third quarter of 2013. During the fourth quarter, the new cyanidation circuit had an average throughput of 904 tpd (based on 38 operating days) and the flotation circuit was operating at an average of 1,196 tpd (based on 74 operating days out of 92 calendar days) for a combined average operating rate of 2,100 tpd. The flotation circuit processed 88,468 tonnes during the fourth quarter with an average silver grade of 226 g/t and a 69% recovery of silver. The new cyanidation circuit processed a total of 34,370 tonnes with an average head grade of 164 g/t silver and recoveries of 60%. As the Company continues to ramp up the cyanidation to 2,000 tpd, it is expected that grades and recoveries will come closer to rates indicated in the Pre-feasibility Study (PFS) dated August 20, 2012.

Cash cost per ounce for the fourth quarter was $12.16, an increase of $2.87 compared to $9.29 in the previous quarter. The increase in cash cost per ounce is primarily attributed to additional diesel and generator rental costs due to delays in the construction of the power line, additional smelting and refining costs due to impurities and some inefficiencies related to early stage operations. Cash cost per ounce is expected to decline in mid-2014 as the power line is completed. In addition, the Company is working diligently to stabilize the milling and metallurgy process at Del Toro to assist in further reducing costs.

During late 2013, the Company entered into several option agreements to acquire six adjacent mineral properties, namely the Chalchihuites, Navidad, Milagros, Zaragosa, Santa Clara and Ivone properties. These properties consist of 492 hectares of mineral rights. When fully exercised, the total purchase price will amount to $3.3 million, of which $1.1 million has been paid, $0.6 million is due in 2014, $1.2 million in 2015 and the remaining balance of $0.4 million due over years 2016 and 2017.

La Encantada Silver Mine

A total of 962,505 equivalent ounces of silver were produced at the La Encantada plant during the fourth quarter of 2013. Production in the fourth quarter of 2013 increased 3% compared to the 931,027 equivalent ounces of silver produced in the third quarter of 2013 and decreased by 14% compared to the 1,117,254 equivalent ounces of silver produced in the fourth quarter of 2012.

Since the second quarter of 2013, the planned mix of fresh ore to old tailings being processed through the plant was altered by reducing the tailings feed by almost 50% while increasing the feed of fresh ore. During the fourth quarter of 2013, the ratio consisted of 72% fresh ore and 28% of old tailings with a total throughput averaging 3,042 tpd consisting of an average of 2,202 tpd of fresh mine ore and 840 tpd of old tailings. With the increase of fresh ore from the mine and the reduction of old tailings, the overall cost per tonne of production has increased due to the higher cost of mining from the underground mine compared to the low cost of hauling old tailings to the mill. Total production cost per tonne for La Encantada was $37.49 during the fourth quarter, consistent with the previous quarter, while cash cost per ounce in the current quarter was $10.61 and comparable to the $10.70 in the third quarter of 2013.

In 2014, the Company is planning to upgrade and expand the crushing and grinding areas to allow the underground extraction of fresh mine ore to be increased in the second half of 2014, including the installation of a new 24’ x 14’ ball mill. In addition, beginning in January 2014, the reprocessing of old tailings has been eliminated from the mill feed due to the low metal price environment. This modification is expected to improve both silver recoveries and the head grade at the mill.

La Parrilla Silver Mine

Total production at the La Parrilla mill was 1,151,728 equivalent ounces of silver in the fourth quarter of 2013, which was a decrease of 5% compared to 1,208,635 equivalent ounces in the third quarter of 2013 due to slight decrease in grade and recoveries of silver. Compared to the fourth quarter of 2012, total production increased 24% primarily due to 8% increase in tonnage processed. Cash costs per ounce in the fourth quarter were $6.45 and in-line with the previous quarter.

The Company has now completed 1,057 metres of development and construction of the underground rail haulage level. Due to the reduced budget in development costs, the timeline for the 5,000 metre project has been extended until the end of 2016. When completed, this new haulage and underground electric rail system will consist of 5,000 metres of development and a shaft of 260 vertical metres and will replace the current less efficient above-ground system of trucking ore to the mill. This investment is eventually expected to improve ore logistics, ultimately reducing overall operating costs and thereby delivering higher operating margins from La Parrilla’s complex of mines.

San Martin Silver Mine

Total production in the fourth quarter of 2013 was 313,834 ounces of silver equivalent, a decrease of 17% compared to the 377,816 ounces of silver equivalent produced in the third quarter of 2013, but 17% higher than the 267,635 equivalent ounces of silver produced in the fourth quarter of 2012. Production was negatively affected by some maintenance down time during the expansion into new equipment including the agitation tanks, impacting leaching time and impacting the counter current washing system, resulting in lower recoveries during the fourth quarter.

Cash costs per ounce in the fourth quarter was $13.96, an increase of 35% from compared to $10.34 in the third quarter. The increase in costs was due to a 17% decrease in produced silver ounces due to the lower recoveries experienced during the mechanical issues mentioned above and lower silver grades.

The average head grade was 156 g/t in the fourth quarter of 2013, compared to the 165 g/t in the third quarter of 2013 and 136 g/t in the fourth quarter of 2012. The decrease in the ore grade compared to third quarter of 2013 was due to lower grade in the stopes. The increase in ore grade compared to the same quarter of the prior year was attributed to production from the newly developed Rosarios/Huichola areas.

La Guitarra Silver Mine

During the quarter, total production at the La Guitarra mill was 299,533 equivalent ounces of silver, an increase of 5% compared to the 285,256 ounces produced in the third quarter of 2013 and an increase of 22% compared to the 246,319 ounces in the fourth quarter of 2012.

Cash cost in the fourth quarter was $4.08, which decreased by 28% compared to $5.63 in the third quarter. The decrease in cash costs was primarily attributed to an increase in gold by-product credits and reduction of smelting and refining costs.

The permitting of a 1,000 tpd cyanidation processing facility is currently in the planning and evaluation stage. It is anticipated that permit applications will be submitted to the Mexican authorities during 2014. Once this new processing facility is permitted and fully constructed, production of silver doré bars is anticipated to replace the production of silver/gold concentrates.

2014 GUIDANCE

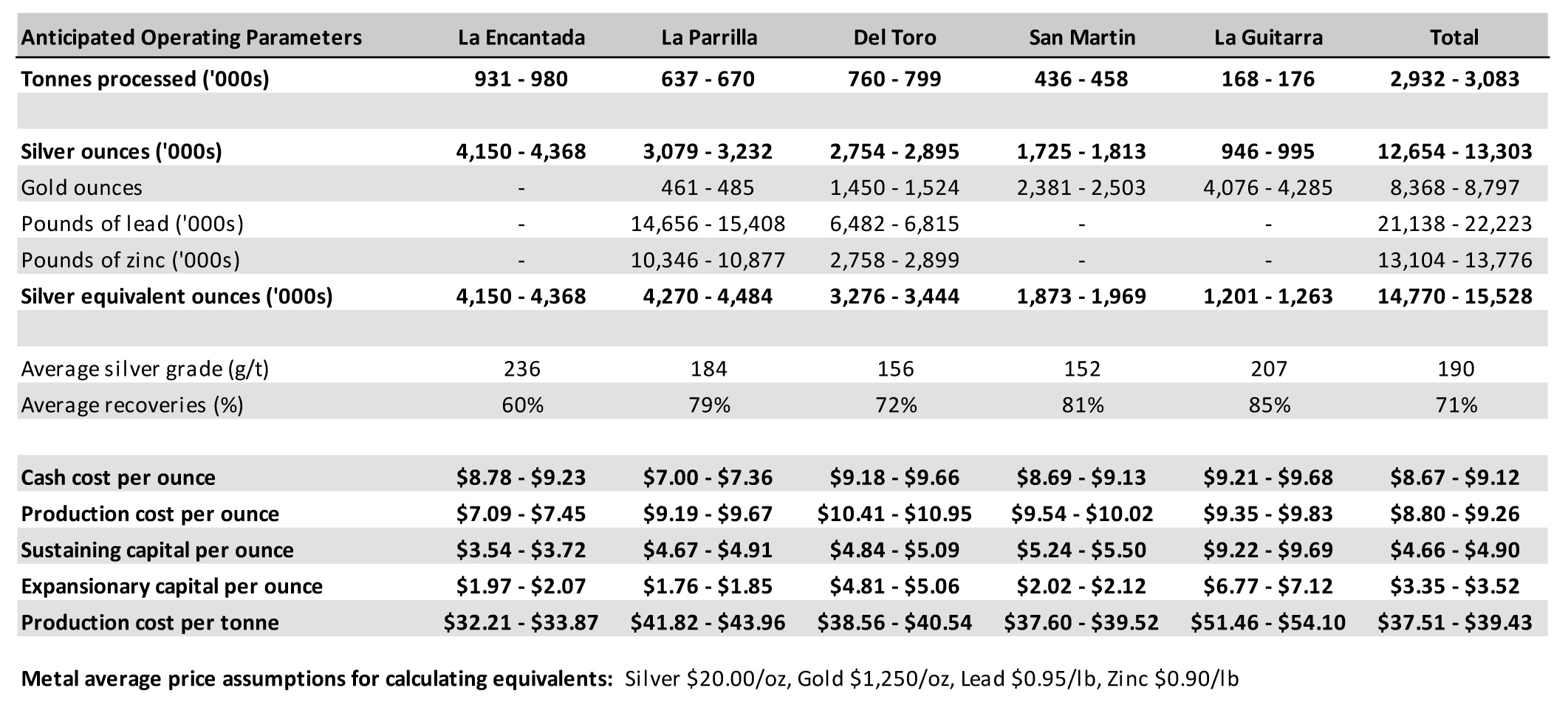

On January 14, 2014, the Company announced 2014 silver production is expected to increase by 19% to 25% to a new operating range of 12.7 to 13.3 million silver ounces (or 14.8 to 15.6 million silver equivalent ounces). All-in sustaining costs are projected to be in the range of $15.87 to $16.69 per payable silver ounce.

The following is a summary of the Company’s 2014 outlook by producing mines:

CONFERENCE CALL AND WEBCAST

A conference call and webcast will be held today, February 26, 2014 at 11:00 a.m. PST (2:00 p.m. EST) to review and discuss the financial results. To participate in the conference call, please dial the following:

| Toll Free Canada & USA: | 1-800-319-4610 |

| Outside of Canada & USA: | 1-604-638-5340 |

| Toll Free Germany: | 0800 180 1954 |

| Toll Free UK: | 0808 101 2791 |

Participants should dial in 10 minutes prior to the conference.

Click on WEBCAST on the First Majestic homepage as a simultaneous audio webcast of the conference call will be posted at www.firstmajestic.com.

First Majestic is a mining company focused on silver production in México and is aggressively pursuing the development of its existing mineral property assets and the pursuit through acquisition of additional mineral assets which contribute to the Company achieving its corporate growth objectives.

FOR FURTHER INFORMATION contact info@firstmajestic.com, visit our website at www.firstmajestic.com or call our toll free number 1.866.529.2807.

FIRST MAJESTIC SILVER CORP.

“signed”

Keith Neumeyer, President & CEO

SPECIAL NOTE REGARDING FORWARD-LOOKING INFORMATION

This news release includes certain “Forward-Looking Statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and applicable Canadian securities laws. When used in this news release, the words “anticipate”, “believe”, “estimate”, “expect”, “target”, “plan”, “forecast”, “may”, “schedule” and similar words or expressions, identify forward-looking statements or information. These forward-looking statements or information relate to, among other things: the price of silver and other metals; the accuracy of mineral reserve and resource estimates and estimates of future production and costs of production at our properties; estimated production rates for silver and other payable metals produced by us, the estimated cost of development of our development projects; the effects of laws, regulations and government policies on our operations, including, without limitation, the laws in Mexico which currently have significant restrictions related to mining; obtaining or maintaining necessary permits, licences and approvals from government authorities; and continued access to necessary infrastructure, including, without limitation, access to power, land, water and roads to carry on activities as planned.

These statements reflect the Company’s current views with respect to future events and are necessarily based upon a number of assumptions and estimates that, while considered reasonable by the Company, are inherently subject to significant business, economic, competitive, political and social uncertainties and contingencies. Many factors, both known and unknown, could cause actual results, performance or achievements to be materially different from the results, performance or achievements that are or may be expressed or implied by such forward-looking statements or information and the Company has made assumptions and estimates based on or related to many of these factors. Such factors include, without limitation: fluctuations in the spot and forward price of silver, gold, base metals or certain other commodities (such as natural gas, fuel oil and electricity); fluctuations in the currency markets (such as the Canadian dollar and Mexican peso versus the U.S. dollar); changes in national and local government, legislation, taxation, controls, regulations and political or economic developments in Canada, Mexico; operating or technical difficulties in connection with mining or development activities; risks and hazards associated with the business of mineral exploration, development and mining (including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins and flooding); risks relating to the credit worthiness or financial condition of suppliers, refiners and other parties with whom the Company does business; inability to obtain adequate insurance to cover risks and hazards; and the presence of laws and regulations that may impose restrictions on mining, including those currently enacted in Mexico; employee relations; relationships with and claims by local communities and indigenous populations; availability and increasing costs associated with mining inputs and labour; the speculative nature of mineral exploration and development, including the risks of obtaining necessary licenses, permits and approvals from government authorities; diminishing quantities or grades of mineral reserves as properties are mined; the Company’s title to properties; and the factors identified under the caption “Risk Factors” in the Company’s Annual Information Form, under the caption “Risks Relating to First Majestic’s Business”.

Investors are cautioned against attributing undue certainty to forward-looking statements or information. Although the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be anticipated, estimated or intended. The Company does not intend, and does not assume any obligation, to update these forward-looking statements or information to reflect changes in assumptions or changes in circumstances or any other events affecting such statements or information, other than as required by applicable law.