First Majestic Reports Second Quarter Financial Results and La Encantada Operational Update

August 11, 2015

VANCOUVER, BRITISH COLUMBIA--(Marketwired - Aug. 11, 2015) - FIRST MAJESTIC SILVER CORP. (TSX:FR)(NYSE:AG)(FRANKFURT:FMV)(BVM:AG) (the "Company" or "First Majestic") is pleased to announce the unaudited interim consolidated financial results of the Company for the second quarter ended June 30, 2015. The full version of the financial statements and the management discussion and analysis can be viewed on the Company's web site at www.firstmajestic.com or on SEDAR at www.sedar.com and on EDGAR at www.sec.gov. All amounts are in U.S. dollars unless stated otherwise.

SECOND QUARTER 2015 FINANCIAL HIGHLIGHTS

- Generated revenues of $54.2 million

- Mine operating earnings amounted to $3.4 million

- Operating cash flows before movements in working capital and taxes of $16.4 million or $0.14 per share

- Net loss after taxes amounted to $2.6 million or per share of ($0.02)

- Produced 3.8 million silver equivalent ounces, including 2.7 million ounces of pure silver

- Total cash cost, net of by-product credits, was $8.74 per payable silver ounce

- All-in sustaining cost ("AISC") was $14.49 per payable silver ounce, a 20% reduction compared to $18.18 per ounce in second quarter of 2014

- Average realized selling price for silver was $16.99 per ounce, compared to the quarterly COMEX average silver price of $16.38 per ounce

- Cash and cash equivalents of $37.7 million held at the end of the quarter

Keith Neumeyer, President and CEO of First Majestic, stated: "Our all-in sustaining cash costs in the first half of 2015 came in at the low end of guidance at $14.18 per ounce, or a 23% reduction compared to $18.46 per ounce in the first half of 2014. Cost reductions at Del Toro have had a great impact on our bottom line with all-in sustaining costs falling to $7.13 per ounce in the first half of the year compared to $21.52 per ounce in the first half of 2014. Additional cost savings are anticipated in the second half of 2015 as we realize higher operational efficiencies at La Encantada due to its recent expansion to 3,000 tpd."

SECOND QUARTER 2015 HIGHLIGHTS

| HIGHLIGHTS | Q2 2015 |

Q1 2015 |

Q/Q Change |

Q4 2014 |

Q3 2014 |

Q2 2014 |

||||||||||

| Operating | ||||||||||||||||

| Ore Processed / Tonnes Milled | 662,637 | 631,609 | 5% | 683,528 | 621,196 | 671,024 | ||||||||||

| Silver Ounces Produced | 2,716,503 | 2,776,855 | (2% | ) | 3,074,567 | 2,680,439 | 3,098,218 | |||||||||

| Silver Equivalent Ounces Produced | 3,802,558 | 3,905,270 | (3% | ) | 4,247,527 | 3,523,536 | 3,855,223 | |||||||||

| Cash Costs per Ounce(1) | $ | 8.74 | $ | 8.22 | 6% | $ | 8.51 | $ | 10.41 | $ | 9.63 | |||||

| All-in Sustaining Cost per Ounce(1) | $ | 14.49 | $ | 13.88 | 4% | $ | 14.43 | $ | 19.89 | $ | 18.18 | |||||

| Total Production Cost per Tonne(1) | $ | 46.80 | $ | 46.90 | (0% | ) | $ | 47.15 | $ | 54.34 | $ | 51.81 | ||||

| Average Realized Silver Price per Ounce ($/eq. oz.)(1) | $ | 16.99 | $ | 17.05 | (0% | ) | $ | 16.30 | $ | 19.10 | $ | 19.59 | ||||

| Financial ($ millions) | ||||||||||||||||

| Revenues | $ | 54.2 | $ | 54.6 | (1% | ) | $ | 72.5 | $ | 40.8 | $ | 66.9 | ||||

| Mine Operating Earnings (2) | $ | 3.4 | $ | 5.0 | (31% | ) | $ | 5.8 | $ | (1.8 | ) | $ | 9.5 | |||

| Net Earnings | $ | (2.6 | ) | $ | (1.1 | ) | (133% | ) | $ | (64.6 | ) | $ | (10.5 | ) | $ | 7.6 |

| Operating Cash Flows before Working Capital and Taxes (2) | $ | 16.4 | $ | 17.3 | (5% | ) | $ | 21.1 | $ | 9.0 | $ | 19.0 | ||||

| Cash and Cash Equivalents | $ | 37.7 | $ | 22.4 | 69% | $ | 40.3 | $ | 34.7 | $ | 66.7 | |||||

| Working Capital (1) | $ | (0.9 | ) | $ | (12.6 | ) | 93% | $ | (2.9 | ) | $ | 11.4 | $ | 46.1 | ||

| Shareholders | ||||||||||||||||

| Earnings per Share ("EPS") - Basic | $ | (0.02 | ) | $ | (0.01 | ) | (127% | ) | $ | (0.55 | ) | $ | (0.09 | ) | $ | 0.06 |

| Adjusted EPS(1) | $ | (0.03 | ) | $ | 0.00 | (845% | ) | $ | 0.04 | $ | (0.04 | ) | $ | 0.02 | ||

| Cash Flow per Share(1) | $ | 0.14 | $ | 0.15 | (8% | ) | $ | 0.18 | $ | 0.08 | $ | 0.16 | ||||

| (1) | The Company reports non‐GAAP measures which include cash costs per ounce, all‐in sustaining cost per ounce, total production cost per ounce, total production cost per tonne, average realized silver price per ounce, working capital, adjusted EPS and cash flow per share. These measures are widely used in the mining industry as a benchmark for performance, but do not have a standardized meaning and may differ from methods used by other companies with similar descriptions. |

| (2) | The Company reports additional GAAP measures which include mine operating earnings and operating cash flows before movements in working capital and income taxes. These additional financial measures are intended to provide additional information and do not have a standardized meaning prescribed by IFRS. |

FINANCIAL REVIEW

The Company generated revenues of $54.2 million for the second quarter of 2015, a decrease of 19% compared to the second quarter of 2014 primarily due to a 13% decrease in average realized silver prices and a 3% decrease in silver equivalent ounces sold. Compared to the prior quarter, revenues decreased 1% primarily due a minor decrease in total production.

Net loss increased by $1.5 million compared to the prior quarter to a loss of $2.6 million, or ($0.02) per share. The loss is primarily related to a $1.5 million non-cash loss on derivatives, prepayment facility and investments.

Mine operating earnings decreased to $3.4 million compared to $5.0 million in the previous quarter. The decrease in mine operating earnings was primarily affected by a decrease in silver equivalent ounces sold.

Cash flows from operations before movements in working capital and income taxes in the quarter totaled $16.4 million or $0.14 per share, compared to $17.3 million or $0.15 per share in the previous quarter. The decrease is due to lower mine operating earnings.

On April 22, 2015, the Company completed the bought deal private placement, issuing 4,620,000 common shares at a price of CAD$6.50 per share for gross proceeds of $24.5 million (CAD$30.0 million), or net proceeds of $23.0 million (CAD$28.1 million) after share issuance costs.

As previously announced on July 27, 2015, the Company entered into a definitive agreement to acquire all of the issued and outstanding shares of SilverCrest for consideration of 0.2769 common shares of First Majestic plus CAD$0.0001 in cash per SilverCrest common share. With this acquisition, SilverCrest's Santa Elena Mine will be First Majestic's sixth producing silver mine, adding further growth potential to the Company's portfolio of Mexican projects and enhances the Company's working capital position. Pending the close of the SilverCrest acquisition, which is expected in early October, the Company plans to revise production and cost estimates and include SilverCrest's Santa Elena Mine in its consolidated operating guidance.

OPERATIONAL HIGHLIGHTS AND UPDATES

Total production for the quarter was 3,802,558 silver equivalent ounces consisting of 2,716,503 ounces of silver, 3,528 ounces of gold, 11,078,235 pounds of lead and 3,824,737 pounds of zinc. The 3% decrease in production compared to the previous quarter was primarily attributed to lower production from Del Toro, which encountered 16% lower silver grades and a decrease in silver recoveries while mining through a lower grade area of the Perseverancia mine, as well as a 9% decrease in production at La Parrilla due to a return to normal zinc grades after encountering exceptionally high zinc grades within the Vacas mine last quarter. The decreases at Del Toro and La Parrilla were partially offset by a 33% improvement in production at La Guitarra due to improved silver and gold grades and a new quarterly production record at San Martin.

At La Encantada, the ramp up to the 3,000 tpd is progressing as planned. The new ball mill averaged 2,889 tpd in the month of July with similar silver grades and recoveries experienced in the prior quarter. With economies of scale resulting from the higher throughput levels, AISC are expected to improve in the second half of the year. In addition, silver grades are expected to remain in the range of 160 g/t to 180 g/t for the remainder of the year.

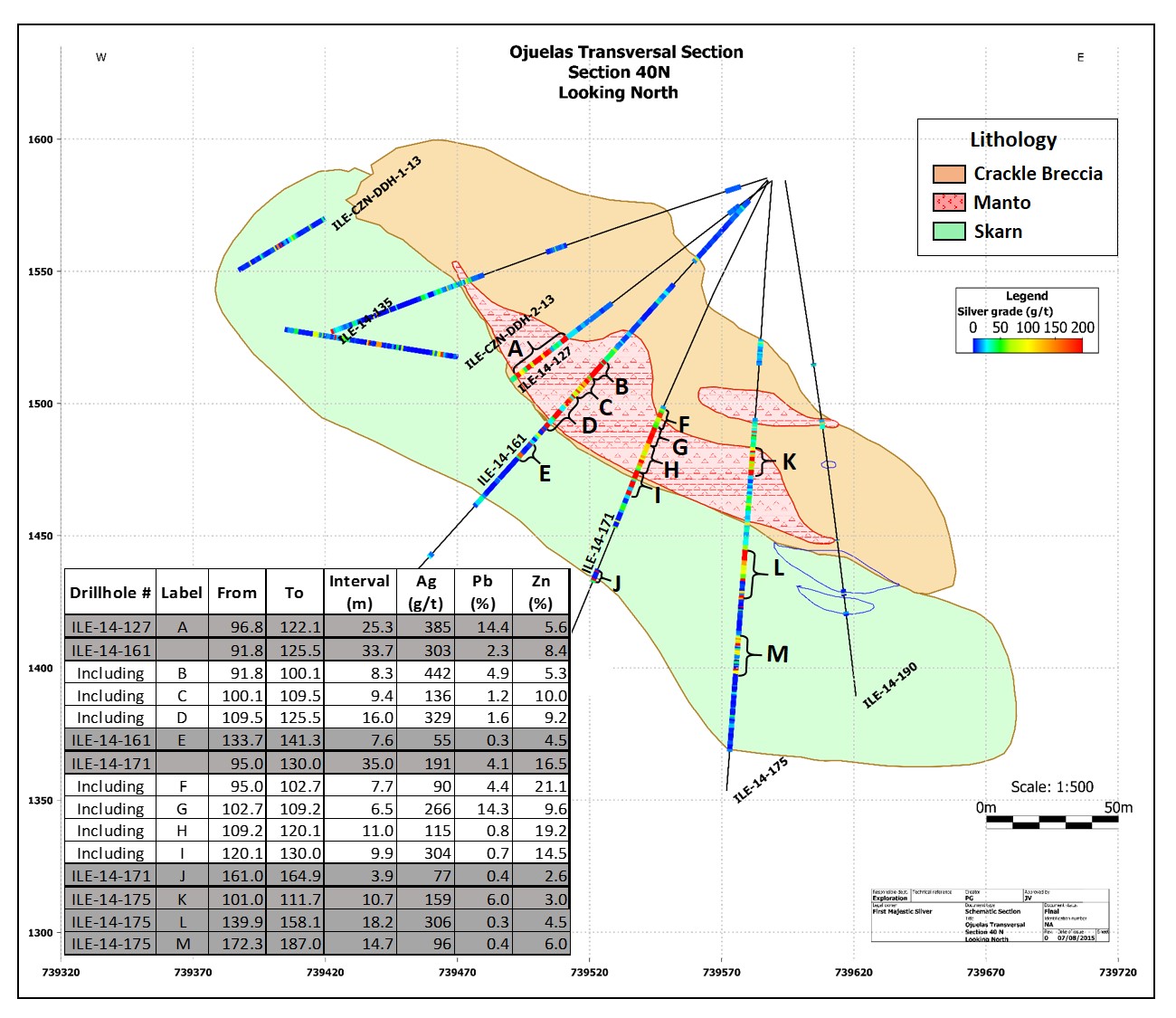

Due to the discovery of the Ojuelas ore body at La Encantada, the Company is planning to release an updated NI 43-101 Technical Report in the fourth quarter of 2015. Since the initial discovery in late 2014, over 6,350 metres in 28 holes have been completed in and around the Ojuelas ore body. It is expected that all 28 holes, pending final assays, will be considered in the updated NI 43-101 Technical Report which will incorporate a cut-off date of August 6, 2015. Two drill rigs are currently active and continue to infill drill and explore the open ends to the north and south flanks.

The cross section shown in figure 1 is part of the ongoing exploration program being carried out by the Company and includes numerous holes and assay results. Highlights includes hole ILE 14-161 which intersected 34 metres of oxide mineralization with average grades of 303 g/t silver, 2.3% lead, 8.4% zinc and very low manganese. Also, suphide mineralization containing high levels of lead and zinc was also discovered in the scarn directly below the oxide manto. Samples are undergoing metallurgical testing and the results will be released in the upcoming Technical Report.

To view Figure 1: La Encantada Silver Mine, Ojuela Manto, please visit the following link: http://media3.marketwire.com/docs/1020904-F1.jpg

{kind=link}

COSTS AND CAPITAL EXPENDITURES

Cash cost per ounce (after by-product credits) for the quarter was $8.74 per payable ounce of silver, down from $9.63 per ounce in the second quarter of 2014. Compared to the previous quarter, the cash cost per ounce increased 6% primarily due to annual union bonuses at Del Toro and La Parrilla and less by-product credits at La Parrilla due to the decrease in zinc production. Cash costs at all other mines either improved or were consistent when compared to the previous quarter.

As shown in the table below, consolidated AISC in the second quarter was $14.49 per payable silver ounce, a 4% increase compared to $13.88 per ounce in the previous quarter and a 20% reduction compared to $18.18 per ounce in the second quarter of 2014. With the La Encantada mill expansion now complete plus higher silver and gold grades at San Martin and La Guitarra, the Company expects AISC to further improve in the second half of the year.

The following table contains the mine by mine AISC from the second quarter of 2015 compared to the previous quarter and the second quarter of 2014.

| All-in Sustaining Costs (per Payable Silver Ounce) | ||||||||

| Mine | Q2 2015 |

Q1 2015 |

Q/Q change |

Q2 2014 |

Y/Y change |

|||

| La Encantada | $ | 18.32 | $ | 17.85 | 3% | $ | 14.25 | 29% |

| La Parrilla | $ | 14.48 | $ | 12.58 | 15% | $ | 11.42 | 27% |

| Del Toro | $ | 6.97 | $ | 7.25 | -4% | $ | 20.44 | -66% |

| San Martin | $ | 9.62 | $ | 8.69 | 11% | $ | 15.89 | -39% |

| La Guitarra | $ | 13.32 | $ | 17.71 | -25% | $ | 23.39 | -43% |

| Total: | $ | 14.49 | $ | 13.88 | 4% | $ | 18.18 | -20% |

Capital expenditures in the second quarter were $17.4 million, primarily consisting of $4.2 million at La Encantada, $4.0 million at La Parrilla, $3.8 million at Del Toro, $2.8 million at San Martin and $2.1 million at La Guitarra. Compared to the previous quarter, capital expenditures increased 10% primarily due to higher investment at La Encantada to complete the plant expansion. In the first half of 2015, the Company invested a total of $33.1 million towards capital expenditures, or approximately $4.7 million below budget, and expects the second half of 2015 to achieve similar savings due to lower sustaining costs and fewer expansionary investments.

Mr. Ramon Mendoza Reyes, Vice President Technical Services for First Majestic, is a "qualified person" as such term is defined under National Instrument 43-101, and has reviewed and approved the technical information disclosed in this news release.

ABOUT FIRST MAJESTIC

First Majestic is a mining company focused on silver production in México and is aggressively pursuing the development of its existing mineral property assets and the pursuit through acquisition of additional mineral assets which contribute to the Company achieving its corporate growth objectives.

FIRST MAJESTIC SILVER CORP.

Keith Neumeyer, President & CEO

SPECIAL NOTE REGARDING FORWARD-LOOKING INFORMATION

This news release includes certain "Forward-Looking Statements" within the meaning of the United States Private Securities Litigation Reform Act of 1995 and applicable Canadian securities laws. When used in this news release, the words "anticipate", "believe", "estimate", "expect", "target", "plan", "forecast", "may", "schedule" and similar words or expressions, identify forward-looking statements or information. These forward-looking statements or information relate to, among other things: the price of silver and other metals; the accuracy of mineral reserve and resource estimates and estimates of future production and costs of production at our properties; estimated production rates for silver and other payable metals produced by us, the estimated cost of development of our development projects; the effects of laws, regulations and government policies on our operations, including, without limitation, the laws in Mexico which currently have significant restrictions related to mining; obtaining or maintaining necessary permits, licences and approvals from government authorities; and continued access to necessary infrastructure, including, without limitation, access to power, land, water and roads to carry on activities as planned.

These statements reflect the Company's current views with respect to future events and are necessarily based upon a number of assumptions and estimates that, while considered reasonable by the Company, are inherently subject to significant business, economic, competitive, political and social uncertainties and contingencies. Many factors, both known and unknown, could cause actual results, performance or achievements to be materially different from the results, performance or achievements that are or may be expressed or implied by such forward-looking statements or information and the Company has made assumptions and estimates based on or related to many of these factors. Such factors include, without limitation: fluctuations in the spot and forward price of silver, gold, base metals or certain other commodities (such as natural gas, fuel oil and electricity); fluctuations in the currency markets (such as the Canadian dollar and Mexican peso versus the U.S. dollar); changes in national and local government, legislation, taxation, controls, regulations and political or economic developments in Canada, Mexico; operating or technical difficulties in connection with mining or development activities; risks and hazards associated with the business of mineral exploration, development and mining (including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins and flooding); risks relating to the credit worthiness or financial condition of suppliers, refiners and other parties with whom the Company does business; inability to obtain adequate insurance to cover risks and hazards; and the presence of laws and regulations that may impose restrictions on mining, including those currently enacted in Mexico; employee relations; relationships with and claims by local communities and indigenous populations; availability and increasing costs associated with mining inputs and labour; the speculative nature of mineral exploration and development, including the risks of obtaining necessary licenses, permits and approvals from government authorities; diminishing quantities or grades of mineral reserves as properties are mined; the Company's title to properties; and the factors identified under the caption "Risk Factors" in the Company's Annual Information Form, under the caption "Risks Relating to First Majestic's Business".

Investors are cautioned against attributing undue certainty to forward-looking statements or information. Although the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be anticipated, estimated or intended. The Company does not intend, and does not assume any obligation, to update these forward-looking statements or information to reflect changes in assumptions or changes in circumstances or any other events affecting such statements or information, other than as required by applicable law.